Unknown Facts About Mortgage Investment Corporation

Unknown Facts About Mortgage Investment Corporation

Blog Article

All About Mortgage Investment Corporation

Table of ContentsAbout Mortgage Investment CorporationThe Greatest Guide To Mortgage Investment CorporationExcitement About Mortgage Investment CorporationWhat Does Mortgage Investment Corporation Mean?The smart Trick of Mortgage Investment Corporation That Nobody is Discussing

Does the MICs credit rating committee evaluation each home loan? In many circumstances, home loan brokers handle MICs. The broker ought to not serve as a member of the credit report committee, as this puts him/her in a straight problem of passion considered that brokers normally make a payment for putting the home loans. 3. Do the directors, members of debt board and fund supervisor have their own funds spent? Although an of course to this inquiry does not supply a risk-free financial investment, it must supply some enhanced safety and security if assessed along with various other prudent lending plans.Is the MIC levered? The financial organization will accept certain home loans had by the MIC as protection for a line of credit score.

It is crucial that an accounting professional conversant with MICs prepare these statements. Thank you Mr. Shewan & Mr.

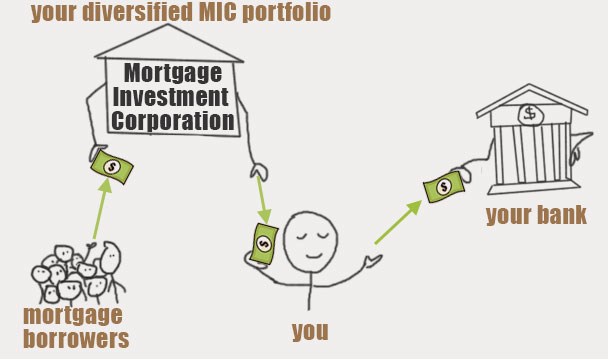

Last updated: Upgraded 14, 2018 Few investments are financial investments advantageous as a Mortgage Investment Home mortgage (Firm), when it comes to returns and tax benefits. Because of their business structure, MICs do not pay revenue tax and are legally mandated to distribute all of their revenues to financiers.

This does not suggest there are not dangers, however, typically talking, no matter what the more comprehensive supply market is doing, the Canadian realty market, particularly major urban locations like Toronto, Vancouver, and Montreal performs well. A MIC is a company formed under the regulations set out in the Earnings Tax Obligation Act, Area 130.1.

The MIC makes income from those mortgages on rate of interest charges and general costs. The actual appeal of a Mortgage Investment Firm is the return it provides capitalists compared to various other set earnings investments. You will certainly have no trouble locating a GIC that pays 2% for a 1 year term, as federal government bonds are equally as low.

Get This Report about Mortgage Investment Corporation

There are strict requirements under the Earnings Tax Obligation Act that a corporation need to meet before it qualifies as a MIC. A MIC must be a Canadian firm and it should invest its funds in home loans. MICs are not permitted to handle or develop real estate property. That said, there are times when the MIC winds up possessing the mortgaged residential property as a result of repossession, sale contract, and so on.

A MIC will gain rate of interest revenue from home loans and any kind of cash the MIC has in the bank. As long as 100% of the profits/dividends are offered to shareholders, the MIC does not pay any type of revenue tax. Rather of the MIC paying tax on the interest it gains, shareholders are in charge of any tax.

About Mortgage Investment Corporation

And Deferred Strategies do not pay any type of tax obligation on the rate of interest they are approximated to receive - Mortgage Investment Corporation. That said, Get More Information those that hold TFSAs and annuitants of RRSPs or RRIFs may be struck with certain penalty tax obligations if the investment in the MIC is taken into consideration to be a "restricted investment" according to copyright's special info tax code

They will certainly ensure you have actually discovered a Home loan Investment Company with "competent financial investment" status. If the MIC certifies, it could be extremely beneficial come tax obligation time considering that the MIC does not pay tax on the rate of interest earnings and neither does the Deferred Plan. Extra extensively, if the MIC stops working to fulfill the requirements established out by the Income Tax Act, the MICs earnings will certainly be taxed before it obtains dispersed to shareholders, decreasing returns substantially.

It shows up both the actual estate and supply markets in copyright are at all time highs Meanwhile returns on bonds and GICs are still near document lows. Even cash is shedding its appeal since power and food rates have actually pushed the inflation rate to a helpful resources multi-year high.

The Basic Principles Of Mortgage Investment Corporation

Lots of difficult functioning Canadians that desire to get a home can not get home loans from standard banks because perhaps they're self employed, or don't have an established credit rating background. Or possibly they desire a brief term financing to develop a big residential property or make some improvements. Financial institutions have a tendency to ignore these potential borrowers because self used Canadians don't have stable incomes.

Report this page